Who should be the next Federal Reserve chair? If it were my decision, first I would try to talk Ben Bernanke out of leaving, since he is the closest thing to a “Depression scientist” that has ever been in the job. And, despite the constraints on any chair of a bankers’ organization, he was the most resistant to austerity measures of all the major central banks, possibly excepting China’s.

The domain of the Federal Reserve is monetary policy: monitoring and managing the supply of money and credit in the economy with a mission of full employment and low inflation. Sometimes these missions are asynchronous, or even in conflict. Bernanke leaned more toward the full employment mission of the Fed than any of his predecessors. Historically the Fed has been accused of leaning more toward inflation fighting than job creation. That is easily explained by the natural fear of bankers, the Fed’s strongest constituency, that inflation erodes the values of their loan assets. But sometimes – like now – modest inflation can be a good thing. Interest rates have been near zero since the financial crisis that began the current depression. Yet corporations and hedge funds are hoarding billions in reserves. Inflation can persuade those who are hoarding capital to put it in circulation.

However, one of the chief lessons of the current depression is that monetary policy did nothing to stop the crisis, and, beyond insuring cheap borrowing rates, has had a limited impact on recovery, though things could have turned out much worse had Bernanke not taken the aggressive actions he did. Bernanke repeatedly urged Congress to provide stronger fiscal stimulus to the economy, the primary Keynesian tool to fight depressions.

Fiscal policy includes both taxing and spending policy. While latter day Keynesians recognize monetary policy as a more powerful tool than it was viewed in Keynes’ time, they still, like Keynes, require the government to make up declines in aggregate demand with public works, services or simple payments (unemployment, welfare services, food stamps, Social Security, Medicare, Medicaid, military). A World War II scale of public investment (120 percent of GDP at the time) and stimulus are often cited as the key factor in finally ending the Great Depression.

But there is a problem with the theoretical fiscal remedies: barring cataclysm or war, the class politics of providing sufficient stimulus is nearly impossible politically, especially when so many institutions – Congress, for example – have been captured by corporate and billionaire interests. The truth is that neither monetary nor fiscal fixes are working to either prevent or recover from depressions.

As Paul Krugman indirectly advised in his blog this week, we need to find someone who understands the limits of both monetary and real life fiscal policy. He writes:

At the very least it means that we need “macroprudential” policies -regulations and taxes designed to limit the risk of crisis -even during good years, because we now know that we can’t count on an effective cleanup when crisis strikes. And I don’t just mean banking regulation…. the logic of this argument calls for policies that discourage leverage in general, capital controls to limit foreign borrowing, and more.

In layman terms, this is equivalent to saying the U.S. economy needs more socialism, more industrial policy, and a rollback of corporate power over the political institutions. Strong medicine – even to provide a framework for recovery in the capitalist sectors of the economy!

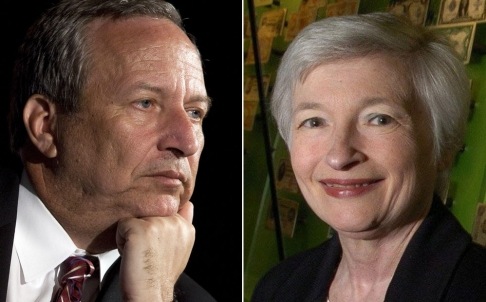

So what does this say about who the next Fed chair should be? The president clearly wants a successor to Bernanke who will maintain the emphasis on jobs over inflation. He thinks Larry Summers is that person. Many others support Janet Yellen, current vice chair of the Fed, who would be the Fed’s first woman chair. Both are eminently qualified Keynesians, both supporters of Bernanke’s policies, although Yellen was somewhat less enthusiastic about financial deregulation than Summers during the tech boom years. At least until unemployment gets significantly lower than the current official rate of 7.5 percent, and perhaps until there is some improvement in workforce participation rates, he wants another Bernanke.

Like Bernie Sanders and others, I would love to see a candidate like Nobel-winning economist Joe Stiglitz get the job. No one better understands the direction economic policy needs to go. Whether that means he could be an effective leader of the Fed is another question. Stiglitz angered many in the 90s when he took on the austerity priests in the World Bank. Being proved right may not have repaired the political and ideological chasms between him and the institution he would be called on to lead.

It is true that Summers bought into the fast money liberalization on Wall Street during the tech boom that contributed to the terrible financial meltdown in 2007. Some say that disqualifies him to be Fed chair. Maybe. He has confessed the errors of that policy. But he is also a first class economist a bit to the left of Bernanke, and a track record of being effective in the hardball environment of bankers and Washington politics.

The Fed will never be a bastion of progressivism. But we need to divide the bosses to move forward. Perhaps the best we can hope for now is to have a Fed chair that will help effect THAT task.

Photo: Larry Summers, left, and Janet Yellen are the two possible candidates to take over the chair of the Federal Reserve.

CONTRIBUTOR

MOST POPULAR TODAY

Ohio: Franklin County treasurer attends Netanyahu meeting, steps up Israel Bond purchases

After months of denial, U.S. admits to running Ukraine biolabs

Hold the communism, please: SFMOMA’s Diego Rivera exhibit downplays artist’s radical politics

“Trail of Tears Walk” commemorates Native Americans’ forced removal

‘Warning! This product supports genocide’: Michigan group aims to educate consumers

Comments