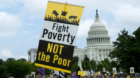

The ink isn’t dry on President Obama’s plan to protect consumers from financial predators and toughen regulation of Wall Street yet already the bankers are digging in to stop any real change.

Edward Yingling, chief executive officer of the American Bankers Association, complained Obama’s plan for a new Consumer Financial Protection Agency (CFPA) may “go well beyond consumer protection.” The banking industry, he warned, will fight to block it or water it down.

He branded Obama’s proposal “so vast and controversial that it will be extremely difficult to enact and will create great uncertainty in the financial markets,” as if foreclosure and bankruptcy for millions of homeowners and the collapse of GM is not “uncertainty.”

Obama’s plan leaves the Federal Reserve, Securities and Exchange Commission (SEC) and other regulatory agencies in charge of overseeing financial markets while increasing their enforcement powers. Yet Yingling said, falsely, that Obama “needlessly rips apart all the existing agencies.”

Ernest Patrikis, former chief legal counsel for AIG protested that Obama’s call for higher capitalization requirements for financial institutions deemed “too big to fail” will cut into profits.

“Stronger capital standards are really going to be an issue,” he warned. “It all becomes a cost factor.” This from a legal eagle who was on AIG’s payroll as it gamed the market, pushed the insurance giant into insolvency, and cost taxpayers $175 billion in bailouts.

The Hedge Fund Association griped that Obama’s requirement that all hedge funds register with the SEC is “unduly burdensome” and “could have a negative impact on the hedge fund industry and the U.S. economy.”

Critics observed that the quick thumbs-down by the bank lobby shows just how lacking Wall Street is in any sense of responsibility for the catastrophe they have inflicted on the nation and the world with their unbridled greed and runaway predatory practices. For them it is full-speed ahead and damn the torpedos.

Yet Obama’s proposals are moderate, some would say, to a fault. Dean Baker, co-director of the Center for Economic Policy Research, author of “Plunder and Blunder: The Rise and Fall of the Bubble Economy,” said the biggest problem with Obama’s plan is that it blames the financial crisis on a lack of adequate regulatory powers. No, Baker argues, the Fed had plenty of enforcement power but “opted not to use their power to rein in the housing bubble.”

He cites arguments in the 88 page white paper released by the White House. That document, he charges “has largely worked to hide the centrality of the housing bubble to the crisis.”

Even if there had been no subprime loans, and credit default swaps “but the housing bubble still had grown to $8 trillion, we would still be in pretty much the same economic situation that we are in today,” Baker said.

“Residential construction would have collapsed due to a huge glut in the housing market and consumption would have plunged as a result of the loss of $8 trillion in household debt,” Baker said. “The fundamental picture is a very simple one of a collapsed bubble causing demand to plummet.”

Baker is pointing the factors even deeper than deregulation as an explanation of the collapse. He does not spell it out in the article posted on Truthout. But those factors are well-known.

The “glut” of unsold homes is a case of what Karl Marx called “overproduction,” an enormous buildup of goods that working people did not have the wherewithal to buy. It is the fruit of decades of de-industrialization, the collapse of manufacturing and the export of millions of union-wage jobs abroad, union-busting and a steady decline in workers’ real wages.

For a time, the economy was kept going through credit—much of it at ruinously high interest rates—until the balloon of consumer debt finally burst. The implication is the restoring regulation must be accompanied by policies that provide jobs with a living income. It’s one reason the labor movement welcomes Obama’s “good jobs, green jobs” agenda. It is also why they are pushing for enactment of the Employee Free Choice Act (EFCA), strongly supported by Obama, to make it easier for workers to join unions and bargain for higher wages and benefits.

Tom McMahon, acting director of Americans United for Change, one of 200 organizations affiliated with Americans for Financial Reform, hailed Obama’s proposals as “the most sweeping changes in a generation.”

For too long, he added, “we have let Wall Street write their own rules, playing games with our money. It’s our homes, our retirement funds, our kids college tuition that have been hurt because no one was watching the big banks. President Obama wants to put someone on our side, looking out for our interests. We need a system that will protect our pocketbooks while putting the economy back on a strong, solid foundation.”