It is easy to be in a gloomy mood about the economy. After a weak and lopsided recovery heavily favoring the capitalist class, the economy looks to be on the cusp of a new downturn. The much talked about double dip is knocking on the door.

The signs are everywhere.

The housing market is in the throes of another slide downward. Both housing prices and startups are down while foreclosures are up.

Consumer spending limps along too, as working people postpone purchases and pay down their debt.

Economic growth rates are paltry, failing to meet earlier very modest projections.

Credit remains tight as banks are reluctant to lend.

Investment lags as businesses, awash in trillions of dollars in investible funds and underutilized production capacity, are reluctant to sink money in new plant and equipment as long as demand for goods and services falters.

Export markets remain weak as well, despite the fall in the dollar’s value on international currency markets. And there is little hope that this will improve as much of the world – and Europe in particular – is in a similar economic predicament.

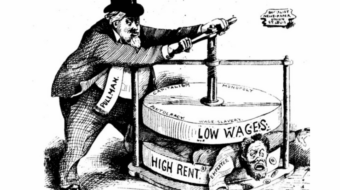

Real wages also are flat, continuing a nearly 40-year trend and aggravating the insufficiency of consumer demand.

Worst of all, the jobless rate is 9.1 percent officially. And unofficially, unemployment is roughly 15 percent. All together 25 million are either unemployed or underemployed and people of color, women and young workers experience the highest rates.

If the prognosis for the short run is bad for everybody but U.S. transnational corporations and banks, whose profits are up, the outlook is no better for the longer run.

Many economists see no easy solution to the financial crisis and the Great Recession. In a recent column, the former top economic advisor for the Obama administration, Lawrence Summers, writes that we run the danger of a lost decade much like Japan, if we don’t stimulate the demand side of the economic equation – in other words, boost consumers’ pocketbooks through jobs and steady incomes.

In these circumstances, the overarching question is: Where will the stimulus come from? What is required to throw the economy and job growth on an upward trajectory?

There is only one answer to this question at this moment: the federal government.

But the problem is that much of the nation’s political and economic elite have no stomach for an expansion of public spending, such as a massive jobs and infrastructure bill.

Instead, calls for austerity fill the media and the political corridors of power. The most insistent voices come from right-wing Republicans who, if they had their way, would withdraw more than a trillion dollars from the economy. In their burial ground would be not only Medicare, Medicaid and Social Security, but also any hope of economic recovery for the foreseeable future.

To make matters worse, the austerity bug has bitten the Obama administration and many Democrats too. While their deficit reduction plans are more modest than the Republicans’ and contain proposals to increase taxes on wealthy corporations and families, the White House and many Democrats on Capitol Hill have put job creation and stimulus spending on the back burner in favor of trickle-down economics.

But cuts, modest or deep-going, are exactly the wrong medicine for a faltering economy. It’s akin to pouring gasoline on a fire. Rather than withdraw money from the economy, additional money should be injected into it.

Our national debt in the longer term is a problem, but austerity at this moment will only exacerbate a deteriorating economy and postpone any sustainable solution to national indebtedness.

If we want evidence of the counterproductive character of austerity, we need only look to Europe, where countries that have attempted to solve their financial and economic crisis by way of austerity find themselves in economic quicksand.

We ignore their experience at our peril. Tens of millions need to say, “Stimulate, stimulate.”

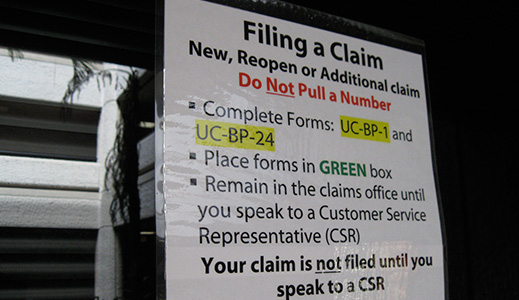

Image: A day at the unemployment office. Bytemarks CC 2.0

CONTRIBUTOR