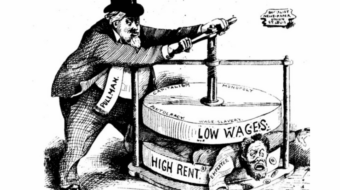

As bailout advances, GOP blocks stimulus for rest of us

The difficulty in sealing a deal to relieve the financial crisis is no surprise. People on Main Street are fuming over the Bush administration’s $700 billion “cash for trash” proposal to bail out Wall Street at taxpayer expense.

An initial slightly modified plan was rejected by lawmakers from both parties in a 205-228 House vote Sept. 29. At press time Senate leaders were moving to modify the plan to win passage.

The plan defeated by the House changed the original Bush plan in a few ways: it broke the $700 billion authorization into installments, added a (weak) mechanism for congressional review, put some caps on pay for CEOs at firms that use the bailout and urged the government, as primary stakeholder in bailed out firms, to try to help people in danger of foreclosure stay in their homes. Senate version increased the insurance for bank accounts from $100,000 to $250,000 and added tax breaks for businesses.

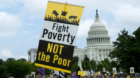

Democrats with labor’s backing introduced a separate economic stimulus package to help ordinary Americans at about one-tenth of the cost of Wall Street’s bailout. Yet, the Republicans blocked it by a filibuster in the Senate Sept. 26. It offered $34.2 billion for job-creating infrastructure projects, including bridge and highway repair, water and sewer projects, public transportation and school repair, and included $14 billion to help states pay their share of Medicaid costs. It also included an extension of unemployment benefits for jobless workers who exhaust their benefits. So far this year the economy has shed more than 600,000 jobs, and more than 9.4 million workers are officially unemployed.

Just as with the war in Iraq, Bush’s Wall Street “rescue” plan tried to lock the federal government into a massive spending spree with no clear exit strategy. He tried to copy the New Deal policy of government intervention in the marketplace without the New Deal’s emphasis on the well being of working people.

For example, he proposed nothing like the Home Owners Loan Corporation organized in the early months of the New Deal. HOLC avoided foreclosures on the homes of working people by purchasing troubled mortgages from banks and reissuing them with more favorable terms.

Yet, such a New Deal-like proposal would have been immediately rejected by him and GOP lawmakers as “socialism” and betrayal of the sacred “free market,” the same reasons they gave in rejecting the Sept. 29 bailout plan.

“[G]iven the ideology of the president and the current Congress, this bailout package might represent the best chance to stop an impending financial meltdown and help prevent substantial fallout to production and employment,” said Lawrence Mishel of the Economic Policy Institute, a labor-oriented think tank. Government inaction is not “an option,” he warned.

Taking a different view, Dean Baker of the Center for Economic and Policy Research argued that the talk of financial collapse is just scare tactics. “There has been a mountain of scare stories and misinformation circulated to push the bailout,” he said. “Yes, banks have tightened credit. Yes, we are in a recession. But the problem is not a freeze up of the banking system. The problem is the collapse of an $8 trillion housing bubble.”

Baker said the “worst case scenario” would be a market “freeze for a few hours” before the “Fed steps in and takes over the major banks,” firing bank executives. Bank shareholders would likely lose “most of their money.” Baker’s estimate seems to be in the minority at this time. Workers may have a stake in a bailout, some argue, with pension funds and 401(k) plans at potential risk.

The presidential election looms large in the bailout machinations. Labor and the people’s movement are putting everything on the line to elect Barack Obama president in order to change the country’s priorities away from Wall Street towards Main Street. A compromise bailout, which is backed by Obama, seems to be a growing political likelihood.

At the same time, the necessity for economic stimulus measures for the working class and small businesses is looming as large as the bailout.

In his New York Times column “Green the Bailout,” Thomas Friedman made the case for investment in “green” manufacturing. “We don’t just need a bailout,” he wrote. “We need a buildup. We need to get back to making stuff, based on real engineering not just financial engineering.”

AFL-CIO President John Sweeney said, “Without a robust economic recovery plan for Main Street, Americans will not trust any financial bailout for Wall Street. Any taxpayer bailout of Wall Street must be balanced with economic relief for ordinary Americans dealing with the economic consequences of Wall Street’s outrageous actions and the government’s own inaction.”

In a letter to Congress on the stalled stimulus package, the AFL-CIO warned:

“The stakes at this time are enormous. If the Wall Street bailout plan ends up squandering hundreds of billions of dollars of the public’s money, the damage will not be limited to the financial system. As a nation we must address the health care crisis, the infrastructure crisis, the energy and environmental crisis, and the jobs crisis. Our future and our children’s future depend on focusing our nation on the challenges in the real economy.

“It is outrageous for President Bush to say we need $700 billion tomorrow to save the banks but it is ‘premature’ to have another stimulus program for the real economy.”

CONTRIBUTOR