The World Bank’s origins go back to the Bretton Woods conference of July 1944, when leaders from 43 nations assembled to start building the global economy in the aftermath of World War II. U.S. Treasury Secretary Henry Morgenthau, hoping to avoid another worldwide depression, called for creation of institutions that would create “a dynamic world community in which the peoples of every nation will be able to realize their potentialities in peace.”

The International Monetary Fund was created at the same time and the two institutions were supposed to facilitate the kind of global economic relations needed to foster peace and security. The IMF would enhance international trade by standardizing monetary policies and maintaining stable exchange rates while providing temporary financial assistance to countries having difficulty with their balance of payments. The World Bank would assist global trade by lending money to war-ravaged and impoverished countries for reconstruction and development, hence its name: International Bank for Reconstruction and Development/World Bank.

In the 1960s the anti-colonial revolution – with moral and material support from the Soviet Union and other socialist states – brought formal political independence to European colonies, particularly in Africa. But the economic tremors of the 1970s brought with them a changed role of the Bank and IMF, who expanded their mission to become the bill collectors of third world debt. In the years since, the dream that national liberation would open new horizons of a better life became a nightmare where hundreds of millions now find themselves sucked into a downward spiral of debt, despair and disease.

Much of the debt accumulated by African countries was built up during the 1970s. In most African countries the debt burden has cut into spending for health care, leaving the annual budget for health care at six or seven dollars per person. But, since there is no provision in international law, countries cannot go bankrupt and must repay their debts no matter the conditions under which they were undertaken. And to make sure of repayment, the IMF and World Bank take virtual control of the economies of borrowing nations by imposing structural adjustment policies (SAPs). That includes South Africa where, in what may be the irony of all ironies, a government headed by Nelson Mandela was required to pay back loans made by a government that helped pay for the repression that kept him in jail for 27 years.

The massive debts that led developing countries to surrender their economy to international banks have accumulated due to predatory lending policies by private banks, loans for infrastructure projects which were poorly conceived or executed; the oil crisis of the 1970s; the dramatic jump in interest rates at the end of the 1970s initiated by the U.S. Federal Reserve Board; and money lost to corruption. They were made worse by wasteful military spending, the cost of civil wars in Angola, Mozambique, the Democratic Republic of the Congo, Rwanda and other countries.

The standard package of IMF “conditionalities” includes:

• Privatization of state-run industries, leading to massive lay-offs with no social security provision and loss of services to remote or poor areas;

• Currency devaluation and export promotion, leading to the soaring cost of imports, land use changed for cash crops; and reliance on international commodity markets to generate the foreign currency needed to service the external debt;

• Raising interest rates to tackle inflation;

• Removal of price controls, and a rapid rise in prices of basic goods and services.

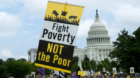

African countries have been among the hardest hit by a global order that has integrated their economies into the global economy as exporters of primary commodities and importers of manufactured goods. These policies have been made even more unequal by neo-liberalism, privatization and deregulation, as well as SAPs imposed by the World Bank and IMF that have combined to generate a level of debt that has crippled Africa’s economies and undermined its ability to determine its own course of economic and social development.

Africa’s manufacturing industries have been destroyed, agricultural production of food and domestic needs is in crisis, public services have been severely weakened and the capacity of African governments to institute policies in support of balanced and equitable national development, emasculated. The costs associated with these have fallen disproportionately on workers, peasants and small producers, with particularly severe consequences for women and children. The numbers tell the story:

• The poor countries of sub-Saharan Africa – in general, the countries lying south of the Sahara Desert but excluding South Africa – owe more than $200 billion in foreign debt, three times more than they earn annually in exports. About 20 percent of sub-Saharan African countries’ export income goes to service foreign debt.

• Half its people live in poverty and, in many countries, per capita income has fallen to levels below those of the 1970s.

• Africa spends four times more on debt interest payments than on health care.

• Thirty-three of the region’s 44 countries are on the United Nations list of heavily indebted poor countries.

• A combination of climate, AIDS and debt have left about six million people in southern Africa facing critical food shortages, in part because the IMF and World Bank have abandoned all subsidies on maize and fertilizer in Mozambique, Zambia and Malawi. Malawi was also forced to sell off its food reserves, a move that has greatly aggravated a famine and resulted in the death of thousands.

• The government of Zambia spent $37 million on primary school education between 1990 and 1993. During that time it spent $1.3 billion – 1,300 million – on debt repayment.

• Per capita external debt for sub-Saharan Africa is $365. GDP per capita is $308.

• Average real wages decreased in 26 out of 28 African countries during the 1980s.

• African children account for about 40 percent of the world’s infant deaths.

• Forty percent of the sub-Saharan African population suffers from some degree of malnutrition.

Africa, where more than 28 million people live with HIV/AIDS, ranks at the top of the victims list of the pandemic that is sweeping countries in the developing world. In Africa alone, 17 million people have died from AIDS, in part because governments are forced to spend more money servicing their foreign debts than they are able to spend on health.

HIV/AIDS is more than a human tragedy. The United Nations says it is rapidly weakening the economic stability of already fragile markets of the developing world. In its UNAIDS Report, the UN warned the disease is erasing decades of development and pointed to the external debt as one of the most important issues in the fight against HIV and AIDS.

Already, the growth rate in sub-Saharan Africa has fallen by as much as 4 percent and labor productivity has been cut by 50 percent in the countries hardest hit by HIV/AIDS. The UN says that by 2020, more than 20 percent of the workforce may be lost in these countries.

According to the United Nations, debt relief has proven to work in dozens of cases in the battle against HIV/AIDS. Malawi received an initial cut of $28 million in debt repayment and used these funds to finance the purchase of critical drugs for hospitals and health centers, hiring extra staff in primary health centers and training nurses. In Uganda, where the external debt was also reduced, the prevalence of adult HIV declined by 40 percent in two years.

Investment by transnational corporations is at the core of the international economy. Private investment in developing countries grew from $44 billion in 1990 to $256 billion in 1997. U.S. private foreign investment increased by $36 billion annually between 1997 and 2000, far in excess of the $11 billion in official development assistance for 2000. Today 100 transnational corporations control a quarter of all foreign-owned assets.

Capitalist globalization and IMF bailouts, the most recent being the $30 billion loan to Brazil, have distorted economies, reduced self-sufficiency, expanded unsustainable use of natural resources, displaced families and communities and made billions of people dependent on foreign markets.

As far as IMF officials are concerned IMF-orchestrated bailouts serve an even more important purpose – they provide money so that developing countries can pay off their foreign creditors, including private banks. In 1999 the fund contributed almost $18 billion to a U.S. bailout of the Wall Street interests that stood to lose billions with the peso devaluation in Mexico.

The same thing happened with the Asian financial crisis, where BankAmerica, Citibank, J.P. Morgan, Bankers Trust, the Bank of New York and Chase Manhattan had approximately $20 billion in outstanding debt in South Korea. With the loans threatening to go bad, the IMF swooped in, pushed the government to take on debts for failing private sector companies and provided tens of billions of dollars to the government to pay off the debts owed to private lenders.

IMF and World Bank policies are premised on “neo-liberalism,” a set of economic premises that have become widespread during the last quarter century. Although conservative politicians hate political “liberals,” they have no problem with neo-liberalism, meaning economic liberalism. The capitalist crisis of the past 25 years, with its shrinking rates of profit, inspired the corporate elite to revive economic liberalism with its elimination of all controls over business and banking. Therefore the “neo;” the new.

The first clear example of neo-liberalism at work came in Chile after the 1973 coup against the government of Salvador Allende. Other countries followed, including Mexico, where wages declined by as much as 50 percent in the first year of NAFTA while the cost of living rose 80 percent. In the years since, over 20,000 Mexican small businesses have failed and more than 1,000 state-owned enterprises have been privatized.

Nor have we in the United States escaped. Neo-liberalism has brought NAFTA and FTAA as well as Enron and WorldCom and the loss of billions in worker’s 401(k) retirement plans. It is destroying welfare programs, attacking the rights of labor and cutting back on social programs – all in the name of the “market” and “getting the government off our backs.”

The battle that hit the public consciousness in 1999 with the “Battle in Seattle” has since been replicated in countries around the world as people in all walks of life have picked up the torch demanding an end to corporate rule. The organizations that initiated the events of Sept. 27-29 in Washington, D.C., demanding an end to corporate rule, have performed a public service that demands the support of everyone.

Fred Gaboury is a member of the Editorial Board of the People’s Weekly World/Nuestro Mundo and writes frequently on economic, labor and political issues. The author can be reached at fgab708@aol.com

CONTRIBUTOR