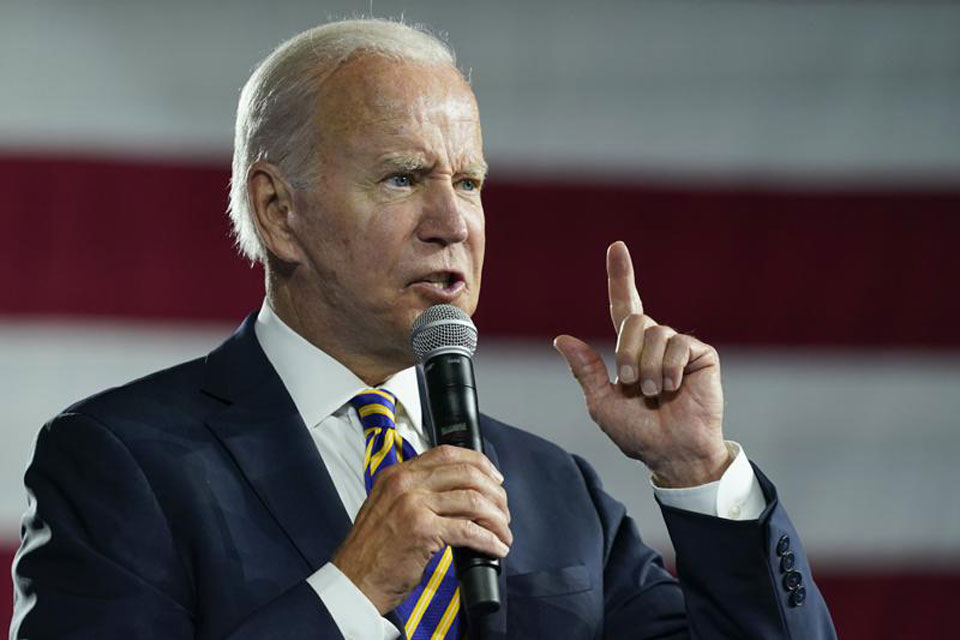

CLEVELAND—Even pensions become political as an election approaches, as Democratic President Joe Biden—for saving them—and congressional Republicans and their right-wing puppeteers—against—proved again in Cleveland on July 6.

Drawing frequent cheers from the capacity union crowd, Biden touted his administration’s—and the congressional Democratic majority’s—success in creating a new structure to rescue financially troubled multi-employer pension plans.

The Republican reaction: Continuing screeches of “a bailout” of union leaders and workers.

The legislation is part of the American Rescue Act and was crafted largely by Sen. Sherrod Brown, D-Ohio. It honors the late Teamsters Local 100 pension leader Butch Lewis. And with a lot of union input from an AFL-CIO working group, it sets up a new structure to let those plans get back on their financial feet.

“Two hundred multiemployer pension plans for two to three million workers and retirees were going insolvent,” Biden told the crowd. “What that means is to those two or three million workers: They faced painful cuts to the benefits they counted on and for the dignified security of retirement.”

Multi-employer plans cover some 11 million workers—and tens of thousands of retirees—ranging from seafarers to musicians to grocery store checkers to construction workers. Now the threat they’d lose their pensions is removed, the president declared.

Union leaders lauded the final rule governing the multi-employer plans, which culminates a long fight to save the pensions of retirees and beneficiaries while not—as the Republicans demanded—clobbering present workers, a form of “robbing Peter to pay Paul.”

“Pensions are more than just a vital part of the retirement plans of millions of Americans, they are a promise made to workers by their employers. And those pensions should not be ripped away after years or decades of hard work. We will keep fighting to protect that promise,” AFL-CIO President Liz Shuler declared.

The problem plans get 30-year federal loan guarantees, as long as those plans get their reorganization blueprints OKd by the Treasury Department and without cutting present recipients’ pensions. That’s directly opposite the Republican scheme for the multi-employer plans, enacted in the dead of night just before the 2014 election.

It featured cuts, big cuts, in workers’ pensions. The Republican tune hasn’t changed.

In the debate over Brown’s bill, the Republicans called multi-employer pensions “rat holes” and the rescue structure a “bailout for union bosses.” Every single Republican opposed the new structure for the pension plans, Biden said.

“People around the country wake up every day wondering whether they’ve saved enough to provide for themselves and their families before they stop working—work at a job that provides basic dignity, a good middle-class job you can raise a family on, a job that provides a dignified retirement and will give you peace of mind,” Biden told the Ironworkers, who cheered him repeatedly.

“Think of all the people…Many of you went to bed at night putting your head on the pillow and saying, ‘Am I going to be all right? Is my family going to be all right? Is my wife or my husband or my child, are they going to be OK?’

“It’s a dignified retirement with your spouse in the home in your community you worked and lived for your whole life. But the reality is for so many people: The goalposts keep moving. Unfortunately, this happens to people who need it most: Working people.

“A lot of politicians like to talk about how they’re going to do something about it. Well, I’m here today to say we’ve done something about it” by fixing the problem.

“I campaigned to restore the backbone of this country—the middle class and unions—because I know this: The middle class built American unions, built the middle class today. I’m keeping the promise” of pensions, “one of the most significant achievements union workers and retirees have received in over 50 years. And that’s not hyperbole.”

In a Zoom press briefing in D.C., top officials of the Labor Department and the Pension Benefit Guaranty Corp. said the new law already rescued 27 multi-employer plans, with three more applications pending. It’ll also keep functioning through 2051. PBGC steps in when a single-employer or multi-employer plan can’t make payments or when corporate bankruptcy wipes out pensions. Final rules for multi-employer plans take effect August 8.

And the Teamsters’ Central and Southern States Multi-Employer Plan, the largest plan endangered by the 2008 crash, has set up an application website for individual workers to get information and apply to participate in its rescue.

The 2014 Republican law, which this measure replaces, forced pension plan boards to keep their plans—which had been financially hammered by the 2008 financier-caused Great Recession—to cut present pensioners’ payouts by 40% or more.

In the press briefing, PBGC Director Gordon Hartogensis added plans forced to make such cuts by 2014 will be “a priority group” for the PBGC and the loan guarantees, thus getting a big chance to make their retirees and beneficiaries whole.

And to ensure safer plan investments in the future, he added, multi-employer plans would be able to invest up to one-third of workers’ pension contributions “in return-seeking assets in publicly traded” common stock and equity funds. But they must invest the other two-thirds in “investment-grade bonds.”

Besides Shuler, other union leaders agreed the new pension plan rules protect workers the multi-employer plans cover.

North America’s Building Trades Unions President Sean McGarvey called the final rules “yet another example showing the Biden-Harris Administration’s commitment to strengthening the economic security of middle-class families across the country.

“This pivotal piece…will directly aid millions of American workers, retirees, and families who faced significant pension benefit cuts, as they will now receive the full benefits they worked years to accumulate. Prior to this critical relief, over 200 plans were on pace to become insolvent.”

The new program “will right the ship and provide funding” workers need “to retire with the security and dignity they earned while saving taxpayers tens of billions of dollars in lost federal tax revenue and future social safety net costs.”

“This long-overdue pension relief legislation provides relief to troubled multiemployer pension plans with NO CUTS to earned benefits,” the Machinists summarized. It “protects the integrity of healthy multiemployer plans, saves the PBGC and strengthens the pension system overall. The legislation contains NO provisions to harm healthy plans.”

The Republican and right-wing reaction? Screams of “a taxpayer-funded bailout of a select group of failing and insolvent, privately managed multi-employer retirement plans.” That’s yet another Republican lie: Multi-employer pension plan boards are split between workers’ reps and bosses’ reps.

The Republican “solution” for workers who could lose part or all of their pensions? Silence. Says Rep. Virginia Foxx, R-N.C., who would take over the House Education and Labor Committee chair if her party wins the House this fall: “Reform” the PBGC, period. About the only “solution” the Republicans didn’t suggest was a lawsuit to overturn the pension law and the rules, as they’ve done with other Biden initiatives.

Instead, the Republicans would ban new plan participants, Foxx said, leaving current workers out in the cold with no pensions, though she conveniently omitted that. And let PBGC “reform” the pension plan boards, too, she said—code words for putting the pensions under corporate control.

CONTRIBUTOR

MOST POPULAR TODAY

Tenth Street Freedmantown: The forgotten Texas town founded by emancipated slaves

What do Unitarian Universalists, communists, anarchists, and socialists have in common?

‘Waiting in the Wings’ theater review: Women led play boldly tackles taboos on death and old age

Amid supply chain crises, Trump administration targets occupied Western Sahara