Greek Prime Minister George Papandreou managed to get a parliamentary vote of confidence Tuesday, June 21. This makes it more likely that Greece can receive a $17 billion installment on an emergency $156 billion bailout loan that was agreed on by its European trading partners last year, and get a new bailout this year. However, these things are not certain; the only thing that is certain is that Greek workers will take a hit and there will be intensified class struggle in the months to come.

The vote in parliament was called by Papandreou, because the troika of institutions that are in charge of the bailouts, namely the European Union, the European Central Bank and the International Monetary Fund, demanded it as a condition for continuing payments on the 2010 bailout and considering another.

It was a foregone conclusion that the opposition, including both the right-wing New Democratic Party and the Communist Party (KKE) and others on the left would vote “no”. The only thing that was in doubt was whether Papandreou’s own Pan-Hellenic Socialist Party (PASOK) would hold together under party discipline, or whether enough PASOK deputies would defect and vote against the measure, possibly triggering elections that the right opposition would surely win, and also putting the bailout arrangements in severe doubt.

At any rate, the vote went 155 to 143 with two abstentions, in the 300-member parliament. The PASOK caucus voted along strict party lines, and no opposition deputy from either left or right voted for the confidence resolution. It had been thought that some of the more left-leaning PASOK deputies might break with Papandreou on the vote. However, at the last minute, he gave them an excuse for voting for the measure by means of what many feel was a largely cosmetic cabinet reshuffle. Next week, he will ask for another parliamentary vote on specific austerity plans. To get the $17 billion, he has to get approval for these measures by July 3.

Now what? In the weeks leading to the vote, tens of thousands of Greeks were in the street demonstrating against the austerity program. Protests have been led by the Communist Party and the PAME labor federation in which it plays a leadership role, but also by other unions, including ones affiliated with the government’s own party, student organizations and increasingly by masses of people connected up through social media. Greek labor has announced a two-day general strike for next week, with more actions to come.

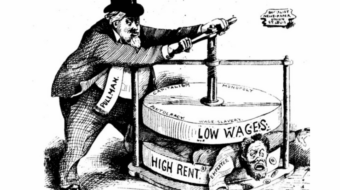

Greek workers see the PASOK government as selling out their interests in favor of their country’s own tax evading super-rich as well as wealthy foreign bankers. They are angry that their own politicians and business elites, with the connivance of Wall Street’s Goldman Sachs, contrived to conceal the degree to which the country’s sovereign debt was getting beyond what Euro zone rules permit, until it was too late, and now they, the workers, have to pay for the damage.

The austerity program includes a fire sale privatization of many important government assets, to the tune of more than $70 billion, which were built up over the years at great cost to the Greek people, including the key seaport facilities of Piraeus and Thessaloniki, plus railways and other public properties. Pensions and government wages will be slashed. Public services will be drastically reduced. Taxes will also be increased, with the Value Added Tax going up a colossal 23 percent. The goal is to reduce expenditures by $40 billion in a country of 11.2 million people with a 2010 Gross Domestic Product of $356 billion.

And nobody is certain that these austerity measures will not worsen instead of improving the situation. Taking money out of the pockets of ordinary Greeks, and laying them off by the thousands, seems to be a strange way of reviving the nation’s economy. But alternatives, such as a restructuring of the debt by stretching out payments over a longer period of time or forcing major bondholders to accept reduced returns, are excluded by the attitudes of the lenders. Although the German government, nervous about the implications of a possible complete default by Greece, has shown some signs of flexibility, the French government and the European Central Bank have been adamant in insisting that austerity is the only condition under which credit will continue to be extended. French Finance Minister Christine Lagarde, who is the front-runner to replace Dominique Strauss-Kahn as head of the IMF, also hinted that she would take a hard line. And it is not a foregone conclusion that Greece will be able to pay its next installment on its debts, in mid July. It may yet default.

Another alternative would have been to sharply devalue the national currency, which would have made Greek exports and also the key sector of tourism more attractive. But Greece cannot do that, having abandoned its own currency for the Euro, which it shares with 26 other countries, including much wealthier ones, who have no desire to devalue.

The bond-rating agency Standard and Poor’s, meanwhile, cut Greece’s rating to CCC, the lowest of any Western European country.

CONTRIBUTOR