Some folks hoped last year that President Obama would consider Paul Volcker for the top job at Treasury because the former Federal Reserve Board chair had come forward in recent years as a vocal critic of those raking in the money on Wall Street.

When everything went bust with the economy in 2008 Volcker blamed the global financial meltdown on the wild, unregulated chase after personal wealth then going full steam in the world of high finance.

The White House gave the Treasury job instead to Timothy Geithner, widely seen as a Wall Street-friendly guy. Volcker was put in charge of the White House Economic Recovery Advisory Board, which, some said, was like being put on ice – never to be heard from again.

That was then. This is now.

Last week, with Volcker at his side and Geithner in a corner, barely visible to the cameras, President Obama called for new regulations that directly challenge the power of the banks.

The president’s strong backing for what he calls the “Volcker rule” plants him on the side of Main Street and in opposition to the Wall Street marauders who have so totally robbed the people.

The proposal from the former Fed chairman essentially restores the 1930s Glass-Steagall banking regulations that, for so long, helped prevent another Great Depression. It involves separating the activities of commercial banks, entrusted with the deposits of working people, from the gambling of the financial high rollers who are presumably dealing not with the peoples’ money but with funds from wealthy investors.

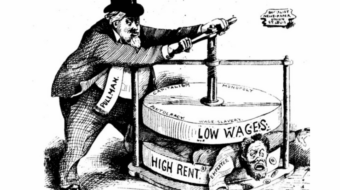

The Roosevelt-era reforms were intended to heavily regulate and insure commercial banks to protect the savings of ordinary folks.

The thinking was that rich investors willing to take risks could fend for themselves and if their wheeling and dealing went bad there would be no innocent victims requiring a government rescue.

All of this worked the way it was supposed to until Ronald Reagan made the first move to change things in 1987 by replacing Volcker with Alan Greenspan, a man who shared Reagan’s belief in totally “unfettered” free markets. The deal involved leaders of both major parties, however, and was finally sealed with the repeal of Glass-Steagall in 1999, when President Clinton signed it into law.

A lot of folks feel the move by Obama has come not a moment too soon.

There is increased worry about the ever-intensifying concentration of wealth at the top and the continuing party on Wall Street.

The seriousness of the situation is underlined in a report issued last week by the congressional Joint Committee on Taxation.

In 2010, the tax panel says, 1 million taxpayers will report incomes over $500,000. These 1 million will earn $241 billion more in income this year than the 80 million taxpayers who will take home less than $40,000 each.

We know the congressional panel is striking at a sensitive nerve as we observe the effort under way on Wall Street this week to paint itself as a bunch now sorry for its sins.

The CEO of Goldman Sachs announced that his company would devote only $16.2 billion to the pay pool for its 32,500 employees, “far less than the $20 billion plus that financial analysts had predicted,” he said.

He also boasted that Goldman is devoting only 35.8 percent of its record 2009 revenue to pay. (Last year it was 48 percent, he reminded everyone.) David Viniar, Goldman’s chief finance officer, said, “We are not deaf to the calls for restraint, and we heard them.”

The Goldman definition of “restraint” means that the “average” employee will be left with a mere $498,153 this year. What they don’t mention is that only a handful will see anything near a half million dollars. The top few are making so much that it pulls up the “average.” The clerks and receptionists, as usual, will earn a relative pittance.

What is really outrageous, however, is that less than a year after the bailout by the people the details of how much is going to whom are unavailable.

There is no place where this reporter or anyone else can go to look for the information about how much that handful of top dogs at Goldman is really getting. We have to wait until later this year when New York State Attorney General Andrew Cuomo will release his analysis of bank payouts.

One key Goldman-Sachs shareholder, however, is unwilling to wait.

The Southeastern Pennsylvania Transportation Authority – the public agency that runs mass transit in the Philadelphia area and that just signed a new contract with its union-represented workers after it forced them into a six-day strike last year – has filed suit against Goldman executives for their ongoing bonus grab.

The Philly investors are warning that no one should buy the Goldman argument that it has already paid back to the Treasury the $10 billion taxpayers gave it. They note that the bank received another $43.4 billion of direct benefit from other bailout programs that has never been reimbursed.

What’s probably the most worrisome for Goldman, however, is that it is operating now in a country where not only some of its investors but the nation’s president and the broad majority of the people are on to its game.

Popular support for taking on Wall Street is soaring even faster than the president’s recent improvement in the polls. A recent Washington Post-ABC News poll found that 73 percent of Americans would support “a special tax on bonuses over $1 million.”

A CBS poll shows that by a 72-19 percent margin Americans feel the federal bailout has benefited “mostly just a few big investors and people who work on Wall Street.”

CONTRIBUTOR