One would think that the near meltdown of financial markets and the larger economy only a few years ago would have dampened Wall Street’s appetite for risky money-making strategies.

But the revelation that JPMorgan Chase lost more than $2 billion (reports say it could be twice as much in the end) in what was essentially speculative trading suggests that Wall Street has learned little.

Indeed one has to ask if Wall Street has learned anything at all. But then again: why would they?

For one thing, Morgan Chase and other banks of its size can still count on federal intervention with taxpayer dollars to bail them out rather than let them go “belly up.” So why not make big, risky bets?

For another thing, the bank titans of the financial world are in the business of profit making, pure and simple. To do that requires that they pursue financial manipulations and speculations, which can, when successful, result in enormous financial rewards in executive compensation and bank profits – or, when unsuccessful, as we are painfully learning, bring down the economy.

In the immediate aftermath of the collapse of financial markets four years ago, placing “too big to fail” banks under public control or breaking these same banks into smaller units were part of the public conversation.

Both measures, however, were rejected by the Obama administration, the Federal Reserve and Congress. Instead, Dodd-Frank, a far from robust financial reform bill that contains rules (some still being written) to regulate financial institutions, was embraced and became law.

Since then, Wall Street and its K Street gang have been lobbying Congress and other Washington insiders to either strike out, rewrite, or water down any regulatory rules in the bill that impede their financial shenanigans.

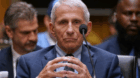

At the head of this lobbying effort is none other than the much “celebrated” Jamie Dimon, CEO of JPMorgan Chase. More than anybody else, he is leading the charge against Dodd-Frank and its modest regulations. Wall Street, he argues, can regulate itself. Right!

His claims have been echoed by leading Republicans, including Mitt Romney.

Of particular scorn for Dimon is the Volcker rule, named after former Federal Reserve Chairman Paul Volcker. This rule, prohibiting “proprietary trading” (banks using federally insured bank deposits – customer money – in trades for stocks, bonds, currencies, commodities, derivatives, or other financial instruments for the purpose of increasing their own accounts), is at the top of his hit list.

And until a week ago it appeared that Dimon would get his way.

The pressure to reform Wall Street had waned as a bit of stability returned to financial markets.

And in the meantime, Republicans in the House of Representatives have shamelessly introduced eight bills to take the teeth out of Dodd-Frank, including the Volcker rule.

But with the revelation of Morgan Chase’s loss of at least $2 billion as a consequence of speculative trading disguised as “hedging” (insurance that is supposedly designed to protect against potential losses from other investments), proponents of more stringent regulatory reform in Congress and elsewhere have been given a second wind. Their hope is that tougher regulations can be passed now.

But no one should hold their breath. Despite the hue and cry about JPMorgan Chase’s reckless behavior, Wall Street and its friends in Washington are not about to run for cover.

Indeed, as outrage over the reckless actions of Morgan Chase swells, they continue to press their case to eviscerate any restraints on their gambling.

Last week two House committees quietly gave approval to HR 1838, the Swaps Bailout Prevention Act. The bill, which will come to the House floor next month, nullifies one of the positive contributions of Dodd-Frank, the so-called Lincoln rule, which bans any federally insured financial institution, like JPMorgan Chase, from trading in derivatives (derivatives were at the center of speculative manipulations in the last crisis).

In all probability the House, notwithstanding public sentiments to rein in bankers and financiers, will approve the bill. Of course, it will have to go to the Senate where support will be more difficult to garner, although not out of the realm of possibility – which attests to the powerful reach and influence of the nation’s leading financial institutions into both parties.

No matter what the outcome, this episode should teach us that the struggle for minor and major financial/regulatory reform – not to mention turning Wall Street into a public democratically run utility – cannot be left to the politicians – even the best of them. It must become the business of an aroused people. The voices of millions must shake the nation’s capital, and the voting booth on Election Day.

Photo: Bank titans always played rough: J. P. Morgan, founder of J. P. Morgan bank which later became JPMorgan Chase, strikes a photographer with a stick, New York, 1909. Recuerdos de Pandora CC 2.0

CONTRIBUTOR